The End of Growth at All Costs and the Rise of Leaner SaaS Organizations

SaaS is about economics, efficiency, discipline, and proving you can build a real business without setting your money on fire.

But the shift we’re living through didn’t happen because founders suddenly woke up one day and decided to act responsibly.

It happened because B2B SaaS investment was bloated for years, and the entire venture ecosystem eventually forced a correction.

Investors moved away from growth at all costs and toward EBITDA discipline, sustainable unit economics, and, in many cases, even began holding up bootstrapped companies as the new benchmark for what healthy growth actually looks like.

For more than a decade, B2B SaaS lived inside one mindset. Grow at all costs. Raise a huge round. Hire aggressively. Build every team at once. Burn runway, at the cost of growth. Assume the next round will appear.

Venture firms rewarded speed over fundamentals because capital was cheap and the market was expanding.

Those days aren't as common as they once were.

This blog breaks down that shift and explains how the new rules of company building have changed team sizes, hiring decisions, seniority ratios, and operational structure. If you want to understand why the SaaS world in 2025 is nothing like the SaaS world in 2015, this will take you there.

When the Hypergrowth Era Collapsed

Harvard Business Review describes this hypergrowth mindset as a system where founders were incentivized to chase valuation rather than sustainable business performance, especially throughout the 2010s [2].

That world evaporated almost overnight.

When interest rates surged in 2022, tech multiples collapsed and the cost of capital skyrocketed.

Suddenly every founder who had been told to grow faster started hearing the opposite message.

Prove you can make money. Show EBITDA discipline. Extend runway. Bessemer’s State of the Cloud report makes this shift explicit by showing how efficiency metrics replaced vanity metrics as investor priorities starting in 2022 and 2023 [1].

Why Growth at All Costs Worked Until It Didn’t

Let’s be honest. For a long stretch, burning money wasn’t just tolerated. It was celebrated.

If you raised a twenty million Series A, investors expected you to turn around and hire fifty people before the end of the quarter. It looked bold and aggressive. It signaled dominance. It helped justify inflated valuations. And it absolutely didn’t matter whether those hires were necessary.

The logic was simple. Capture the market first. Figure out the business model later.

Recurring revenue models made SaaS predictable enough that investors believed the payoff would eventually catch up with the spending. Capital was so cheap that it created an artificial environment where headcount felt like a strategy rather than an expense.

Then reality changed.

When interest rates increased and public tech multiples crashed, the entire incentive model flipped. The same investors who once pushed founders to grow at all costs started asking questions they had not asked in a decade.

What is your CAC payback? What is your gross margin trend? How much runway remains if fundraising slows? How fast can you reach EBITDA breakeven?

Growth was no longer enough. Efficiency became the requirement.

The Startup World Is Not What It Was 15 Years Ago

If you talk to founders who built companies during the 2010 to 2020 era, they almost always say the same thing. It was easier. It was simpler. The expectations were different.

You didn’t have to prove profitability. You did not need a fully optimized CAC model. You didn’t need a disciplined org chart. You hired aggressively because everyone else did. You raised because everyone else raised. And you assumed the party would last forever, or at least till acquisition..

Compare that to building a SaaS company today.

Founders are expected to show efficiency along with scale.

They’re expected to demonstrate customer economics early.

They are expected to operate leaner for longer.

Venture capital firms in the 2020s are still writing large checks, but they are doing it with a different mindset. They want companies that can survive without endless rounds of funding, companies that can grow with lower burn, companies that can function like real businesses.

This fundamental mindset shift is why team structures are changing so drastically.

What Growth at All Costs Teams Looked Like in the Past

During the height of the hypergrowth era, team sizes were shocking compared to what is considered normal today. And these weren’t giant companies.

Series B also included large engineering teams, deep product layers, and fully built operations departments. By Series C and Series D in the old era, it was normal for headcount to explode far beyond operational necessity because headcount itself was seen as a signal of momentum.

None of this would be considered reasonable today, or at a minimum, rare.

These companies were filled with layers of middle management, redundant roles, early hiring of juniors who required heavy oversight, and bloated organizational charts that made decision making sometimes slow and inefficient.

Efficiency didn’t matter as much as it does now. Burn rate did not matter, as long as you were growing. Valuation and perceived scale mattered.

That entire structure is now obsolete.

What Sustainable Profitability Teams Look Like

Modern SaaS companies are rebuilding their teams with a very different formula.

OpenView’s 2023 SaaS Benchmarks reinforce this shift by showing that the most efficient SaaS companies are operating with materially smaller GTM teams, higher seniority density, and tighter alignment between headcount and revenue impact [3].

They are smaller, more senior, more cross functional, and directly tied to EBITDA impact.

They are built around the assumption that capital efficiency is a competitive advantage, not a limitation. Bessemer’s efficiency research reinforces this trend by showing how companies with leaner GTM and product teams consistently performed better across the downturn years [1].

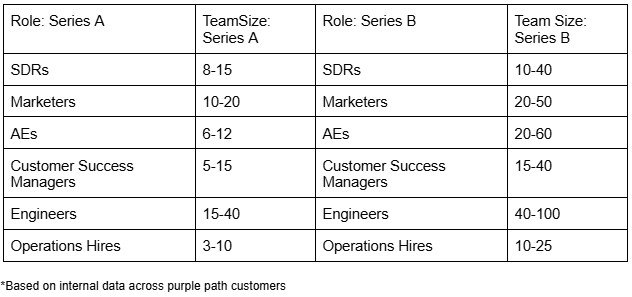

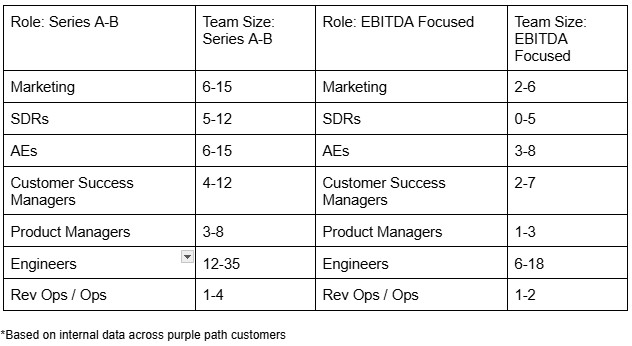

Here is how modern teams typically look at different stages

At pre seed, companies operate with two to five people. Founders, one or two engineers, and maybe a versatile generalist. Marketing is founder led. Every role touches product, customers, or revenue directly.

At seed, teams expand to five to fifteen people. Engineering grows modestly. One or two marketers join.

Customer success appears in a lightweight form. Founder led selling continues, because early revenue requires deep customer proximity. This stage is still about learning and validating rather than scaling.

At Series A and B, teams still grow, but the way they grow has changed. Instead of bloated hiring sprees, companies now add only the functions required to validate and scale their go-to-market model.

Marketing, sales, product, customer success, and engineering all begin to specialize, but the structure is still relatively light and flexible. The goal at this stage is to build repeatability without inflating headcount.

EBITDA-focused teams, however, operate with an entirely different philosophy.

They stay intentionally smaller, more senior, and more cross-functional.

They remove layers instead of adding them.

They rely on automation instead of SDR armies.

They expect every hire to contribute directly to revenue, margin, or product velocity.

Where a Series A/B team adds roles to support scale, an EBITDA-focused team limits roles to protect efficiency.

The contrast is simple. Series A/B teams grow to support the motion. EBITDA-focused teams grow only when the motion demands it. One is about expansion. The other is about precision.

Why Senior to Junior Ratio Now Matters

In the old scaling era, companies hired many juniors because they were cheap and could be managed by a growing army of middle managers.

Modern SaaS companies do not have this luxury. Senior talent is more expensive, but it produces dramatically more output and requires far less oversight.

Most efficient SaaS teams today target a ratio where at least sixty percent of the team is senior level, especially in functions like marketing, engineering, and product. This ensures speed, autonomy, decision quality, and execution ability.

Junior heavy teams create drag. Senior dense teams create velocity, but only when the structure underneath them supports it, because seniors still need experts to execute with them and experts need juniors to support the workload.

The VC Mindset May Have Permanently Shifted

This is one of the most important points founders need to understand.

The funding environment has transformed a bit.

Investors no longer reward hiring sprees, at least for the moment. They reward companies that can survive without constant capital infusion.

They reward efficiency, resilience, and clarity of execution.

Venture firms in the 2020s now rarely want to invest in runway burning machines. They want companies that could be profitable if they needed to be. And they want to see the plan on how you intend to do that.

Sequoia’s “Adapting to Endure” memo captures this clearly by outlining why companies must operate with discipline, efficiency, and strategic focus in a high rate environment [4].

This isn’t going to reverse anytime soon, at least, not with AI being the new growth-at-all-costs movement.

Things have changed.

This is the environment founders must now operate in. At least in the mid-term.

The New Rulebook for Building Teams in 2025 and Beyond

A modern SaaS team design follows a new logic.

And here’s what that looks like:

- Hire slower.

- Hire more experts, even fractionally.

- Build cross functional roles.

- Keep leadership directly involved in execution.

- Track EBITDA earlier.

- Prioritize durable revenue.

- Reduce organizational noise.

- Remove vanity hiring.

- Cut layers.

- Double down on what's working

And build teams that can survive market volatility, not only grow during the best months.

Founders who understand this will move faster with fewer people.

They will build companies that investors trust.

They will avoid the catastrophic burn patterns that took down so many SaaS companies in the post hype correction.

The companies that win over the next decade will not be the biggest teams. They’ll be the most efficient ones.

FAQ

Why did the growth at all costs model slow down?

Because macroeconomic conditions changed. Rising interest rates and falling tech multiples forced investors to prioritize efficient business models instead of runaway burn. Harvard Business Review outlines this shift clearly in its analysis of post 2022 market behavior [1].

Do VCs still invest in SaaS?

Yes. But many of them have radically different expectations. They evaluate profitability levers earlier and focus heavily on sustainable unit economics as described in Bessemer’s State of the Cloud research [2].

What is the biggest difference between teams then and now?

Old SaaS teams were huge and layered. Modern teams are lean, senior heavy, cross functional, and built for EBITDA impact.

Should early stage companies hire SDRs?

Only when founder led sales already works. Many seed and Series A teams now run smaller SDR pods or hybrid roles. But this also depends on the ICP, i.e. enterprise, need for high-ticket solutions)

Is this shift permanent?

Not necessarily. But the cost of capital fundamentally changed the way venture firms evaluate companies.

Sources

Bessemer Venture Partners. State of the Cloud 2024. https://www.bvp.com/atlas/state-of-the-cloud-2024

Harvard Business Review. A Growth at All Costs Mindset Can Stall Your Company. https://hbr.org/2024/04/a-growth-at-all-costs-mindset-can-stall-your-company

OpenView Partners. SaaS Benchmarks 2023. https://openviewpartners.com/blog/2023-saas-benchmarks/

Sequoia Capital. Adapting to Endure. https://www.sequoiacap.com/article/adapting-to-endure/

Andy Culligan

Andy is a fractional CMO, CRO, and marketing advisor who's spent his career getting sales and marketing teams to focus on one thing: commercial results. Before co-founding purple path, he ran marketing for companies including Emarsys, Exponea, Loadfeeder, Censhare, and Luigi's Box.His approach to Account-Based Marketing is no-nonsense, built to motivate teams and drive revenue, not vanity metrics. At purple path, Andy sets the direction and focus for clients' marketing plans, then coaches senior marketers on how to execute fast and get more out of the resources they already have. With deep experience on both the sales and marketing sides, he brings a proactive, personalized approach to every go-to-market strategy he touches.